Property Tracker report reveals affordability of mortgage payments is the biggest barrier to buying a new home

Property Tracker - September 2023

-

Share this page

Share this link via

-

-

Copy URL

-

Katie Wise

-

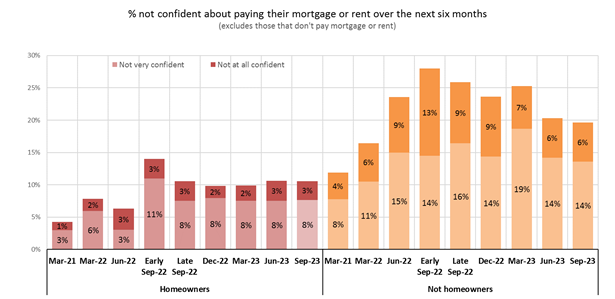

However, most homeowners remain confident they can afford their mortgage payments

-

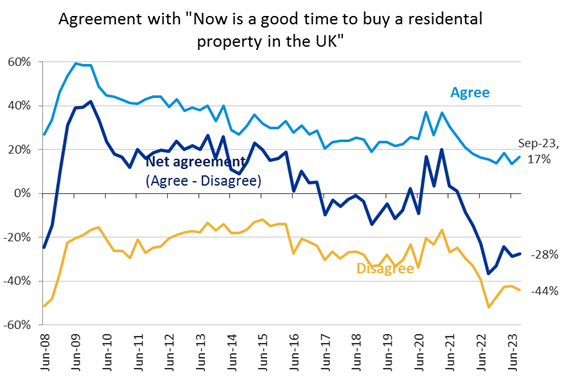

Less than one in five people think now is a good time to buy a home

-

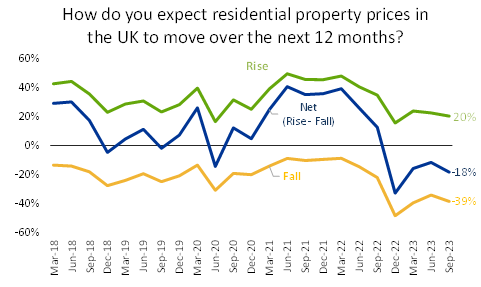

Around one in four think house prices will fall in the next year

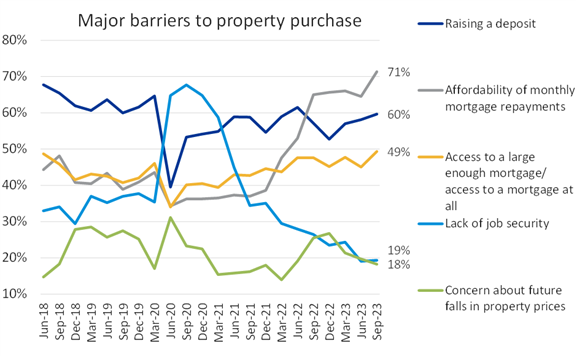

The proportion of people who think mortgage affordability is a barrier to homeownership is now at its highest level in 15 years.

The latest Property Tracker report from the Building Societies Association (BSA) shows that people now think the cost of a mortgage is the biggest obstacle to buying a property when asked to choose their top three barriers.

Impact of Bank Rate rises

Since the first Property Tracker in 2008, raising a deposit has almost always been the biggest barrier to home buying, dropping to second place during the Covid-19 pandemic, when lack of job security was noted as the biggest obstacle.

However, since the Bank of England began hiking interest rates in December 2021, the affordability of monthly mortgage payments as a barrier has grown substantially. Almost three-quarters (71%) of people now cite this when asked for their top three barriers, making it the biggest blocker to home buying. In December 2021, significantly fewer people (39%) mentioned the affordability of mortgage payments as a barrier to buying a home.

Raising a deposit continues to be a significant obstacle to buying a residential property for a major of people (60%). However less than one in five think a lack of job security (19%) and concern about house prices falling (18%) would prevent them from buying a new home.

Affordability concerns

When homeowners were asked about the affordability of their monthly mortgage payments over the next six months, the majority did not express any concern about keeping up with their housing costs.

Almost nine in 10 (87%) mortgage borrowers who gave an answer are not worried about keeping up with their mortgage payments. 10 % are not confident to some extent about maintaining their mortgage payments over the next six months, of which 3% are not at all confident. These figures are unchanged from June and the same as September 2022.

Those who rent their home are a little less assured, with around three-quarters (74%) feeling confident about meeting their housing costs.

Market sentiment

Sentiment in the housing market remains low, but stable. The proportion of people who think now is a good time to buy a property is just 17%, around the same as it was six months ago.

Those who specifically think now is not a good time to buy a new home is considerably higher at 44%, rising to almost seven in 10 (68%) of those who would be first-time homebuyers.

House prices

Market experts are forecasting further house price falls over the coming months. It’s not surprising therefore that one in four (39%) respondents think prices will go down in the next 12 months. However, this is considerably less than in December 2022, when almost half (49%) thought a price fall was likely. One in five (20%) are expecting house prices to rise over the coming year.

Commenting on the findings, Paul Broadhead, Head of Mortgage and Housing Policy at the BSA said:

“Following 13 consecutive Bank Rate rises it’s no surprise that concerns around mortgage affordability have grown, and it is now the biggest obstacle for would-be homebuyers. It is, however, encouraging that the vast majority of homeowners still remain confident that they can maintain their mortgage payments. As inflation figures have finally started to abate, many of these people will now be hoping for the long-awaited respite from rising interest rates.

“Sentiment in the housing market has stabilised, though it remains weak. But we still have some way to go before real confidence returns to the market, particularly as such a high proportion of first-time buyers do not think now is a good time to get on the property ladder.

“Lenders remain conscious that there are a number of families and individuals for whom meeting their mortgage payments is a real worry. They are ready and well equipped to offer practical, tailored support to anyone who may be struggling and would encourage anyone with concerns to contact them as soon as possible, preferably before they miss any payments.”

Ends

Press contacts:

Tanya Jackson, tanya.jackson@bsa.org.uk Tel: 07881 501098

Katie Wise, katie.wise@bsa.org.uk Tel: 020 7520 5904

Notes to Editors:

-

The BSA represents all 42 building societies, as well as 7 of the larger credit unions. Building societies serve around 26 million consumers across the UK and have total assets of over £500 billion. Together with their subsidiaries, they have helped over 3.6 million families and individuals to buy a home with mortgages totalling over £370 billion, representing 23% of total mortgage balances outstanding in the UK. They are also helping over 23 million people build their financial resilience, holding over £362 billion of retail savings, accounting for 19% of all cash savings in the UK. Within this, societies account for 41% of all cash ISA balances.

-

With all of their headquarters outside London, building societies employ around 51,500 full and part-time staff. In addition to digital services, they operate through approximately 1,300 branches, holding a rising share of financial services branches in local communities.

-

For the September Property Tracker survey fieldwork was undertaken between 1-4 September 2023. Total sample size was 2039 adults. The survey was carried out online. The figures have been weighted and are representative of all GB adults (aged 18+). All figures, unless otherwise stated, are from YouGov Plc.

-

When calculating the proportion of those concerned about paying their mortgage or rent it excluded respondents who said ‘not applicable’ or ‘prefer not to say’

-

The proportion agreeing ‘now is a good time to buy’ includes those who agree strongly and those who tend to agree, while the proportion disagreeing includes those who disagree strongly and those who tend to disagree. Respondents who answered 'don't know' are not shown, so percentages do not sum to one hundred.

-

Respondents were given the option to select up to three barriers’ when asked what they think are most likely to stop someone from buying a residential property at the moment.

Appendix