Mortgage lending growth expected to continue in 2026

February market update from the Building Societies Association, including growth outlook, savings and mortgage market.

-

Share this page

Share this link via

-

-

Copy URL

-

Katie Wise

- MPC narrowly votes to hold Bank Rate at 3.75% in February, as inflation risks subside

- Softer labour market and fall in CPI inflation sets up Bank rate cut in March

- Mortgage lending grows 20% in 2025, with further growth expected in 2026

- Households boost savings by £85 billion in 2025, but remains 14% lower compared to 2024

The MPC narrowly voted (5-4) to keep the Bank Rate unchanged at 3.75% in February. This close vote was somewhat unexpected given the tone of previous Bank communications that highlighted the risks around second round inflationary pressures. On balance the MPC judged that the risk from inflation persistence have reduced, whilst the risks around an overly restrictive monetary policy weakening growth and a potential undershoot of the inflation target have remained.

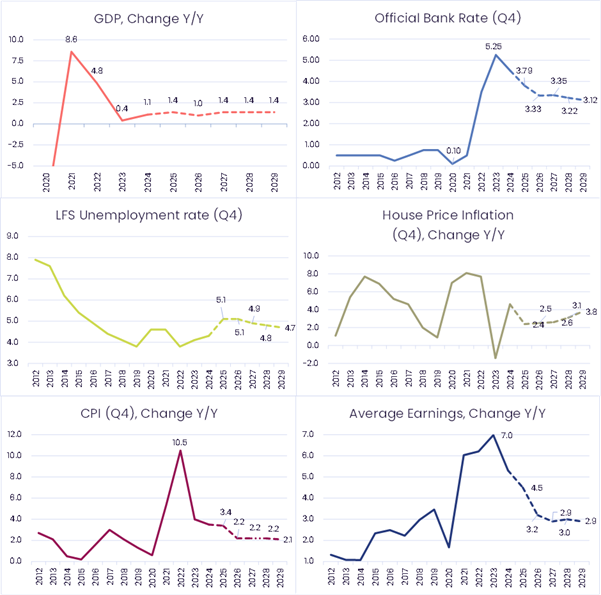

The latest Inflation figures showed further disinflationary evidence with annual CPI inflation falling to 3.0% in January, down sharply from 3.4% in December 2025. Transport and food made the largest downward contributions with annual price inflation in the food category falling from 4.5% to 3.6%.

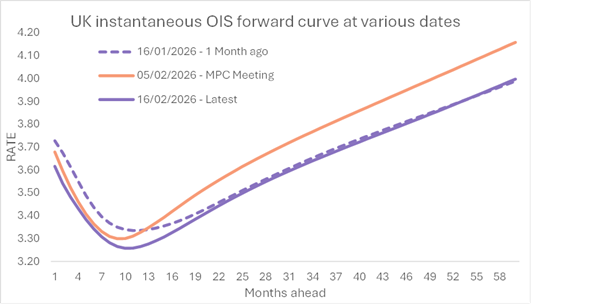

However, the closely watched CPI services annual rate only fell marginally from 4.5% to 4.4%. The February Monetary Policy Report shows CPI inflation is forecast to fall back to its 2.0% target by April 2026 and to 1.7% by Q1 2027. This is based on a market implied Bank Rate that falls to around 3.25% by the end of 2026.

Inflation outlook

The outlook for inflation is weaker compared to the Bank’s November report which largely reflecting the energy bills package introduced in the 2025 Budget and lower gas prices that directly reduces CPI inflation by 0.5 ppts at its peak in Q2 2026. The extent to which this materially impacts inflation expectations and wage setting is yet to be seen and is highly uncertain. The MPC minutes reveal that two of the five members (including Andrew Bailey) who voted to keep rates unchanged believe the lower short term outlook for inflation will mitigate the risks around second-round effects. This could be the case given the recent fall in salient goods such as food.Labour market

ONS data shows further weakening of the labour market. The UK unemployment rate reached a five year high of 5.2% in October to December whilst annual growth in wages fell to 4.2% in the period, down from 4.4% in the three months to November.

Economic outlook

The outlook for the UK economy remains weak, with the Bank reducing its GDP forecasts over the next two years. The latest estimates suggest UK GDP grew by just 1.3% in 2025 – below the Bank’s new lower estimate of 1.4%. Part of this weakness is continued low levels of consumption growth and households saving more.

The average effective mortgage rate has been increasing as people move off low covid-era fixed rates which will continue to weigh on consumption in the near erm. However, there are some positive signs for the economy, with business investment growing by 2.7% in the year to Q4 2025 driven by spending on technology. Although the Bank’s survey points to weaker investment intentions for the future.

There are also tentative signs that productivity growth may finally begin to pick up following years of weakness. This is being supported by the increase in business investment, in particular Artificial Intelligence (AI). However, it is not yet clear to what extend the productivity boosts reflects more a more productive workforce due to AI investment, or simply a reduction in lower paid jobs in hospitality and retail where costs have increased significantly due to the increase in national insurance and minimum wage.

Bank Rate

The likelihood of a cut in Bank Rate in March has increased following the latest data releases with further evidence of disinflation and a softening labour market combined with a weak growth outlook. The latest market rates, which will not capture market movements since the latest data releases, show two further 25 basis point cuts this year, with the first occurring by May.

Mortgage lending grows in 2025 and is expected to continue in 2026

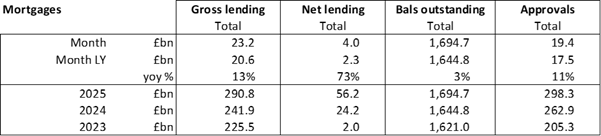

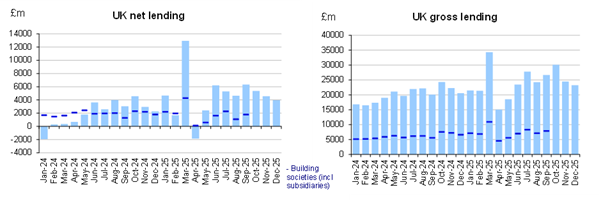

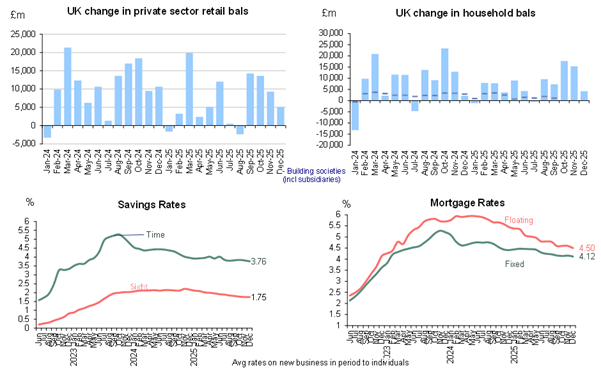

The mortgage market grew by 3.0% in 2025 to reach £1,694.7 billion. This follows a modest, 1.5%, growth in 2024 and 0.0% in 2023. Growth has been supported by real wage growth, falling mortgage rates, modest house price inflation and a relaxation in lending restrictions including on higher LTI lending. £290.8 billion was advanced in 2025, a 20% increase on the £242.0 billion in 2024.

Net lending was £56.2 billion in the year, over double the £24.2 billion in 2024. Growth is expected to continue in 2026 as wage growth remains strong, mortgage rates moderate further, and lenders continue to adjust lending criteria.

There were 1.4 million mortgage approvals in 2025, up 10% compared to 2024. Much of this was driven by the remortgage market which grew by 20% in the year, but also ‘other’ loans which include additional borrowing which grew by 30%. Approvals for new house purchases was up by a modest 2%.

Nationwide reports that affordability for first-time buyers continued to improve in 2025. First-time buyer activity was around 20% higher in the year compared to 2024. A typical first-time buyer with a 20% deposit would have a monthly mortgage payment equivalent to 32% of their take-home pay – slightly above the long-run average of 30% and well below the high of 48% recorded in 1989. The House Price to Earnings ratio for First-time buyers has also dropped to 4.7 which is slightly below its 20-year average.

Nationwide also reported that house prices grew by 0.3% in January 2026, taking the annual rate to 1.0%, up from 0.6% in December 2025.

Average effective variable mortgage rates fell to 4.50% in December 2025, from 4.60% in November 2025, and average effective fixed rates fell to 4.12% in December from 4.16% in November.

Strong savings inflows in 2025 as households exercise caution

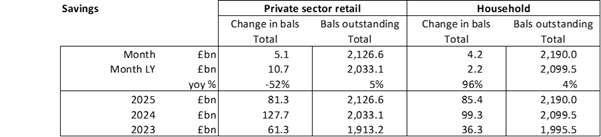

Savings balances increased by £85.4 billion in 2025 following growth in savings balances by £4.2 billion in the final month of the year. Whilst this is 14% lower than the £99.3 billion increase in 2024, it remains high relative to previous (non-pandemic) years and is in line with the relatively high saving ratio as discussed in the first section of this paper. Bank of England survey results suggests households are exercising cation due to higher expectations of job losses and are still concerned over previous high inflation rates.

By mid-February there was £41.9 billion outstanding of TFSME loans from the Bank of England. All original funds drawn down under the scheme have now been repaid, and the outstanding amount are extensions related to Covid loans made by firms in the scheme.

Average effective interest rates on time deposits fell to 3.76% in December from 3.81% in November, and average rates on sight deposits remained unchanged at 1.75%.

December 2025

Average economic forecasts

Average independent forecasts for 2025 & 2026 compiled by HM Treasury in January 2026. Longer term forecasts compiled in November 2025. For full details see the Treasury website.

You may also be interested in...

-

Event

Event

- Thought leadership

MSc Strategic Leadership Programme

Application deadline: Mid-September 2026 Start date: October 2026

-

Research & Reports

Research & Reports

- Banking & Payments

The Social Value of the Building Society Branch Network

The Building Societies Association commissioned RealWorth, a social value consultancy, to carry out a study which examines the social value generated ...

-

Press Release

Press Release

- Banking & Payments

Building societies play vital role in tackling record levels of scams

New research shows building society branches are playing a vital role in protecting customers from scams.

-

Event

- Mortgages & Housing

Annual Meet-up for Mortgage Professionals

Join us for the BSA's Annual Mortgage Meet-up, bringing together mortgage professionals from across the sector for a day of insight, discussion and ne...

-

Press Release

- People

BSA responds to ISA reform anti-circumvention rules & First-time buyer ISA consultation

Government publishes ISA reform anti-circumvention rules & First-time buyer ISA consultation

-

Event

- Mortgages & Housing

Smart Data and the Future Mortgage Journey: From industry insight to organisational impact

A free event hosted by BSA Associate Novus Strategy The mortgage market is changing. For the first time, many of the concepts that have dom...

-

Press Release

- Mortgages & Housing

Building societies back one-in-three first-time buyers and paid £2.1 billion more interest to savers

Figures published today show that building societies and the two mutual-owned banks continued to grow their support for homebuyers and savers in the s...

-

Industry Response

Industry Response

- Prudential Regulation

BSA response to PRA CP5/26 – Modernising the liquidity policy framework

The BSA welcomes the opportunity to comment on CP5/26 on modernising the liquidity policy framework.